From 10 August 2026, self-managed super funds will no longer be able to take out a new loan to buy residential property. The change bans new limited recourse borrowing arrangements for residential real estate only. Existing SMSF property loans are untouched, commercial and business property remain unaffected, and any contract exchanged before the ban takes effect is protected even if settlement happens later.

What Actually Changed

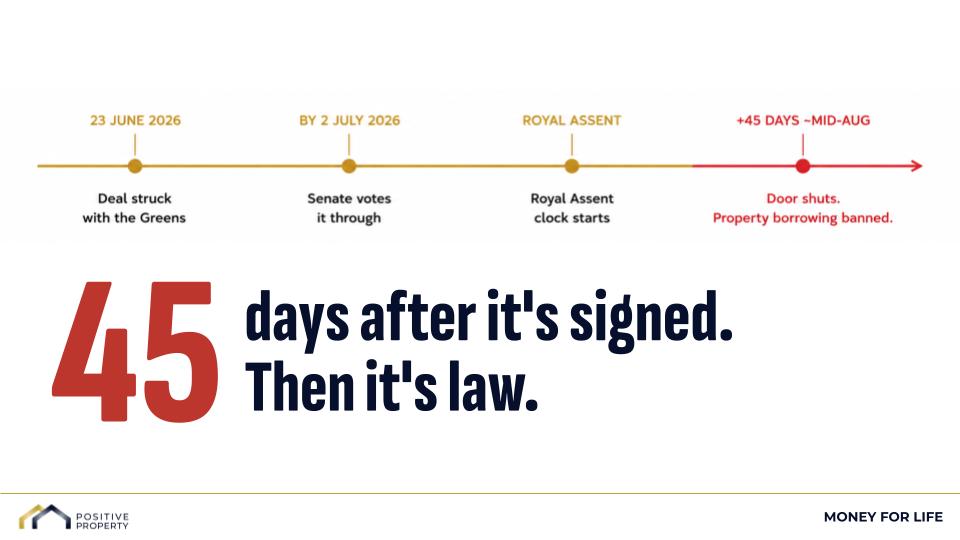

On 23 June 2026, the government agreed to an amendment that bans self-managed super funds from entering new limited recourse borrowing arrangements, known as LRBAs, to purchase residential property. The amendment was moved by Greens Senator Nick McKim and accepted as the price of the Greens’ Senate support for the government’s Treasury Laws Amendment (Tax Reform No. 1) Bill 2026, the legislation that overhauls the capital gains tax discount and tightens negative gearing.

The bill passed both houses and received Royal Assent on 26 June 2026. Under the legislation, the ban commences 45 days after Royal Assent, which puts the practical start date at approximately 10 August 2026.

The change itself is narrow. It inserts a new condition into section 67A of the Superannuation Industry (Supervision) Act, requiring that any property bought using an LRBA be business real property. Residential property no longer qualifies. That is the entire operative change. It does not touch existing arrangements, and it does not touch any other part of how superannuation is taxed or invested.

What’s gone from 10 August 2026:

- New LRBAs used to buy residential property inside an SMSF

What’s unaffected:

- Existing residential LRBAs, which are fully grandfathered

- Refinancing of existing LRBAs

- Commercial and business real property purchased through an LRBA

- Shares, ETFs, and managed funds held inside an SMSF

Why It Happened

The Greens made the LRBA ban a condition of supporting the government’s wider CGT and negative gearing package, arguing that SMSF property purchases risked letting investors sidestep the tougher rules being applied to property held outside super.

Treasurer Jim Chalmers was direct about the scale of the measure when announcing it, telling reporters the change would raise around $50 million over the forward estimates and describing SMSF lending as a small slice of the market: SMSF borrowing accounts for less than one per cent of total residential lending and under half a per cent of new residential lending each year. That figure came from the Treasurer himself, not from industry critics of the deal.

The SMSF Association and several industry bodies have criticised the process, arguing the change was introduced late, without consultation, and goes further than the government’s own negative gearing reforms by ruling out SMSF finance even for new-build purchases. Whatever the merits of that criticism, the numbers Chalmers cited make one thing clear: this measure will not meaningfully move the housing supply or affordability needle. Its function in the deal was political, not structural.

It is also worth noting what this bill did not touch. Superannuation, including SMSFs, was explicitly excluded from the new capital gains tax rules. Super retains its existing concessional treatment: an effective 10 per cent rate on realised gains in accumulation phase, and no capital gains tax at all in pension phase for members over 60. The reform tightens how property is taxed outside super. Inside super, the tax treatment of property itself has not changed. Only the ability to borrow against residential property has.

Who Is Actually Affected

The people this reaches are SMSF trustees who were planning to use borrowed money to buy a residential investment property inside their fund, and had not yet exchanged contracts. That includes tradespeople, small business owners, and anyone building a self-funded retirement strategy around gearing residential property inside super, a strategy that has existed since SMSFs were first permitted to borrow for property purchases in 2010–11.

It does not reach SMSF members who already hold a geared residential property. Those loans stand exactly as they are. It does not reach anyone using an SMSF to hold commercial or business real property, and it does not reach anyone invested in shares, ETFs, or managed funds through their fund.

What It Means in Practice

The date that matters is the contract date, not the settlement date. If contracts are exchanged before the ban commences, the purchase is protected, even if the loan settles months later. This exact question was raised during a recent Positive Property Show livestream, and the distinction matters: an expression of interest does not count, and neither does a deposit on its own. Only an exchanged, signed contract locks the purchase in.

One common misunderstanding is worth correcting directly. Trustees who already hold a geared SMSF property cannot draw on the equity in that property to fund a second purchase before the window closes. The limited recourse structure and the bare trust arrangement underpinning an SMSF loan do not allow that. The only way to access equity in an existing SMSF property is to sell it, repay the existing loan, and reinvest the proceeds, which is a materially different and slower process than simply refinancing.

It is also worth separating this change from a different, unrelated superannuation reform that is often confused with it: Division 296, the additional tax on large super balances. Division 296 applies an extra 15 per cent tax on the proportion of realised superannuation earnings attributable to balances above $3 million.

What to Watch Next

Lenders do not always wait for legislation to take effect before changing their own policy. In 2019, during an earlier period of regulatory scrutiny on SMSF lending, several major lenders exited the SMSF LRBA market ahead of any law change. Whether the same happens here, and how many of the smaller non-bank lenders that currently offer SMSF loans keep the product open through to commencement, remains to be seen. Anyone weighing a purchase should treat 10 August 2026 as the outside limit, not the safe planning date.

If you are weighing a purchase before the window closes, understanding your own borrowing position matters more than the headline. Watch our Free Training to see the strategy thousands of Positive Property members use to build their portfolios.

All figures and dates in are based on the Treasury Laws Amendment (Tax Reform No. 1) Bill 2026 as passed, government and Greens statements at the time of passage, and reporting current as of early July 2026. Legislative detail, ATO guidance, and lender policy may be updated before commencement. Individual circumstances vary and this is general information, not financial or legal advice.

Article Q&A

Can I still buy property inside my SMSF after the ban?

Yes, but only using cash the fund already holds, or by buying business real property using a loan. New borrowed purchases of residential property are banned from 10 August 2026.

What happens to my existing SMSF property loan?

Nothing changes. Existing limited recourse borrowing arrangements are fully grandfathered, and refinancing an existing arrangement is explicitly permitted.

What is the actual deadline to lock in a new SMSF property loan?

Contracts need to be exchanged before the ban commences, expected to be around 10 August 2026. Settlement can occur after that date. An expression of interest or a deposit alone does not secure protection.

Does this affect shares, ETFs, or commercial property in my SMSF?

No. The ban applies only to borrowing for residential property. Shares, ETFs, managed funds, and commercial or business real property are unaffected.