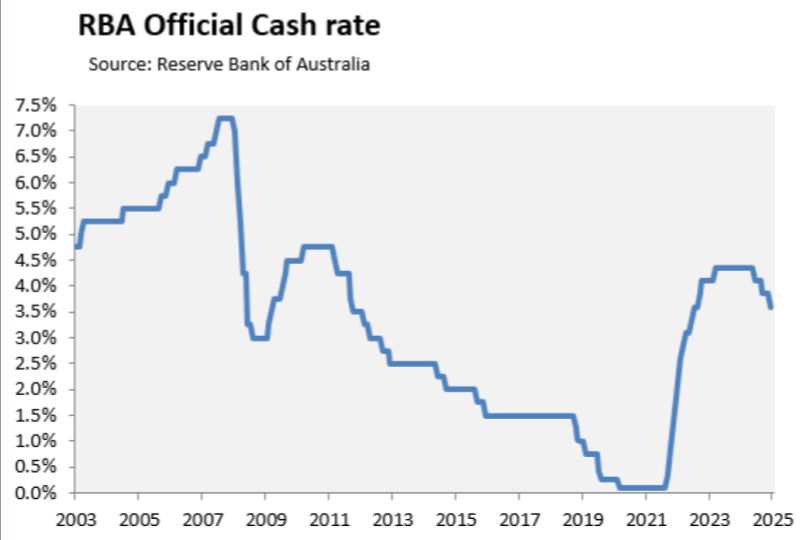

The latest RBA rate cut has made headlines across Australia, dropping the cash rate to 3.6% and prompting the big four banks to slash home loan rates. On the surface, this looks like great news for borrowers. Mortgage repayments fall, borrowing power increases, and the property market gets a jolt of fresh energy.

But beneath the optimism, there are risks that could reshape how buyers and property investors navigate the months ahead. Rate cuts are powerful tools, but they can also spark side effects that catch many Australians off guard. Let’s unpack the three hidden risks behind the latest decision — and what you can do to stay ahead of the curve.

1. Rising Debt Loads

The first hidden risk is also the most immediate. Lower interest rates make borrowing cheaper, but they also encourage households to take on more debt than they can realistically handle.

When repayments shrink, it’s easy to think: “Why not borrow a little extra?” But small increases in borrowing today can snowball into major financial strain tomorrow — especially if the RBA shifts course and rates rise again.

This cycle has played out before in Australia. Borrowers jump at cheaper loans, push their limits, and leave little margin for unexpected changes in income or expenses. The result? Stress, arrears, or even forced sales when the tide turns.

For property investors, this can create a double-edged sword. On one hand, cheaper loans help them expand portfolios. On the other, overleveraging exposes them to cash flow issues if vacancy rates rise or interest rates climb again.

Takeaway: Resist the temptation to max out your borrowing capacity. Build a buffer into every loan decision so you can weather future rate hikes or market shocks.

2. Inflationary Pressures Return

The second risk is less obvious but equally important: inflation. When borrowing costs fall, more buyers enter the market. Demand rises, and in a country already facing housing shortages, that demand quickly pushes up prices.

This creates a feedback loop:

-

Cheaper money fuels demand.

-

Limited supply drives property prices higher.

-

Rising housing costs ripple through the economy, adding pressure to the cost of living.

If inflation spikes again, the RBA may be forced to backtrack with fresh rate hikes. That means today’s relief could be tomorrow’s pain, especially for households who borrowed at their maximum.

For the property market, this risk is especially sharp. An artificial surge in demand can create short-term growth but leave buyers exposed to correction if the RBA needs to cool things down again.

Takeaway: Don’t assume today’s low home loan rates will last forever. Investors and buyers should plan for the possibility of inflationary pressure bringing rate hikes back sooner than expected.

3. Investors Driving Competition

The third hidden risk is competition. Rate cuts don’t just attract first-home buyers — they open the floodgates for seasoned property investors. With lower repayments, investors can leverage their equity to buy more properties, often outbidding younger buyers or those with less capital.

While this creates opportunities for investors to grow wealth, it also risks overheating parts of the market. Suburbs with strong rental demand or new infrastructure projects can suddenly become hotspots, driving prices up rapidly. For first-home buyers, this can be devastating — just as they see affordability improve, investors swoop in and drive values out of reach.

For investors themselves, competition can create another trap: paying too much. When enthusiasm is high, it’s easy to justify stretching beyond fundamentals. That can leave portfolios vulnerable if growth stalls.

Takeaway: Investors should stick to proven strategies — targeting growth corridors, focusing on cash flow, and avoiding emotional purchases. Remember: the best returns often come from buying smart, not buying first.

How to Navigate the Risks

While the RBA rate cut brings challenges, it also creates opportunities for those who approach it with discipline. Here are three strategies to help you stay ahead:

-

Buy with strategy, not emotion. Focus on fundamentals like location, infrastructure, and rental demand instead of chasing hype.

-

Prioritise cash flow. Positive cash-flow properties provide stability and a cushion against future interest rate rises.

-

Think long-term. Property is cyclical. Don’t chase short-term gains — build a portfolio designed to last through market ups and downs.

By focusing on fundamentals and building a long-term plan, investors can protect themselves from the hidden dangers of a rate cut. You can explore more of our property market insights to see how these strategies play out in real time.

The Bigger Picture

Australia’s property market has always been shaped by cycles of rate cuts, rate hikes, and shifting economic forces. Today’s decision from the RBA is just one moment in a longer story. For some, it will spark opportunity; for others, it may trigger financial stress.

What matters most isn’t the headline itself, but how you respond to it. Borrowers who treat this as a chance to plan strategically will benefit. Those who dive in without caution may find themselves facing the very risks we’ve outlined.

Final Thoughts

The RBA rate cut is more than just a number on a chart — it’s a shift that will ripple through the entire housing landscape. While banks lower home loan rates and confidence builds, it’s essential to remember the hidden risks: rising debt loads, inflationary pressure, and investor-driven competition.

Handled wisely, this environment could unlock wealth-building opportunities. Handled recklessly, it could lead to stress and setbacks.

👉 Want the complete analysis, including deeper insights and strategies for today’s market? Listen to the full discussion on Spotify, Apple Podcasts, or watch on YouTube.